销售增长和支出干预的因果归因#

场景#

假设我们有一个在线销售产品的广告商。为了促进销售,他们通过价格促销发放折扣,并通过展示广告和搜索结果页面的赞助广告进行在线推广。为了准备即将到来的业务审查,广告商比较了 2024 年和 2023 年的数据,观察到销售额和产品页面浏览量等关键绩效指标 (KPI) 稳步增长。然而,分析团队想知道是什么因素推动了这种增长,是广告、价格促销,还是仅仅由于购物者趋势带来的自然增长?这些问题的答案对于理解过去的增长至关重要。此外,该广告商希望获得可操作的业务规划建议,例如在投资回报率更高的领域加大投入。在以下场景中,我们将双重使用 DoWhy:首先,恰当地对 KPI 增长驱动因素进行因果归因,以便分析团队以数据驱动的方式理解过去增长的动力。其次,我们根据因果影响估算进行干预,以推导增量投资回报率 (iROI),以便广告商可以预测额外投资带来的未来 KPI 增长。这些因素和 KPI 包括:* dsp_spend:通过展示广告在需求方平台 (DSP) 上的广告支出 * sp_spend:在搜索结果页面上的广告支出,以提升产品排名,便于发现 * discount:通过降价提供的折扣 * special_shopping_event:一个二元变量,表示电商平台是否举办了购物活动,如黑色星期五或网络星期一 * other_shopping_event:一个二元变量,表示电商平台之外的其他购物活动。这可能来自广告商本身,或其在其他平台上的广告活动。* dpv:产品详情页浏览量 * sale:焦点电商平台上的日收入

[1]:

import matplotlib.pyplot as plt

import networkx as nx

import numpy as np

import pandas as pd

from functools import partial

from dowhy import gcm

from dowhy.utils.plotting import plot

from scipy import stats

from statsmodels.stats.multitest import multipletests

gcm.util.general.set_random_seed(0)

%matplotlib inline

1. 探索数据#

首先,让我们加载表示 2023 年和 2024 年支出、折扣、销售额及其他信息的数据。请注意,对于此模拟数据,我们没有改变比较期间的价格折扣分布,因此在随后的归因模型中不应检测到这种变化。

[2]:

df = pd.read_csv('datasets/sales_attribution.csv', index_col=0)

df.head()

[2]:

| dsp_spend | sp_spend | dpv | discount | sale | activity_date | year | quarter | month | special_shopping_event | other_shopping_event | |

|---|---|---|---|---|---|---|---|---|---|---|---|

| 0 | 11864.799390 | 2609.702789 | 54954.823150 | 26167.824599 | 76740.886670 | 2023-01-01 | 2023 | 1 | 1 | 否 | 否 |

| 1 | 11084.057110 | 2568.540570 | 44907.063324 | 22340.009780 | 52480.718941 | 2023-01-02 | 2023 | 1 | 1 | 否 | 否 |

| 2 | 16680.850945 | 2847.576700 | 151643.912564 | 68301.747813 | 628062.966309 | 2023-01-03 | 2023 | 1 | 1 | 否 | 否 |

| 3 | 15473.576264 | 2788.515831 | 121173.343955 | 18906.050402 | 307547.583964 | 2023-01-04 | 2023 | 1 | 1 | 否 | 否 |

| 4 | 10308.414302 | 2523.591011 | 36234.267337 | 18198.689563 | 35602.101926 | 2023-01-05 | 2023 | 1 | 1 | 否 | 否 |

为了将感兴趣的因素因果归因于变化,我们首先需要定义比较的时间段。

[3]:

def generate_new_old_dataframes(df, new_year, new_quarters, new_months, old_year, old_quarters, old_months):

# Filter new data based on year, quarters, and months

new_conditions = (df['year'] == new_year) & (df['quarter'].isin(new_quarters)) & (df['month'].isin(new_months))

df_new = df[new_conditions].copy()

# Filter old data based on year, quarters, and months

old_conditions = (df['year'] == old_year) & (df['quarter'].isin(old_quarters)) & (df['month'].isin(old_months))

df_old = df[old_conditions].copy()

return df_new, df_old

df_new, df_old = generate_new_old_dataframes(df, new_year=2024, new_quarters=[1,2], new_months=[1,2,3,4,5,6], old_year=2023, old_quarters=[1,2], old_months=[1,2,3,4,5,6])

然后我们定义累积分布函数,以便粗略观察两个时期指标的变化。让我们绘制它们

[4]:

def plot_metric_distributions(df_new, df_old, metric_columns):

for metric_column in metric_columns:

fig, ax = plt.subplots()

kde_new = stats.gaussian_kde(df_new[metric_column].dropna())

kde_old = stats.gaussian_kde(df_old[metric_column].dropna())

x_range = np.linspace(

min(df_new[metric_column].min(), df_old[metric_column].min()),

max(df_new[metric_column].max(), df_old[metric_column].max()),

1000

)

ax.plot(x_range, kde_new(x_range), color='#FF6B6B', lw=2, label='After')

ax.plot(x_range, kde_old(x_range), color='#4ECDC4', lw=2, label='Before')

ax.fill_between(x_range, kde_new(x_range), alpha=0.3, color='#FF6B6B')

ax.fill_between(x_range, kde_old(x_range), alpha=0.3, color='#4ECDC4')

ax.set_xlabel(metric_column)

ax.set_ylabel('Density')

ax.set_title(f'Comparison of {metric_column} distribution')

ax.spines['top'].set_visible(False)

ax.spines['right'].set_visible(False)

ax.grid(True, linestyle='--', alpha=0.7)

ax.legend(fontsize=10)

plt.tight_layout()

plt.show()

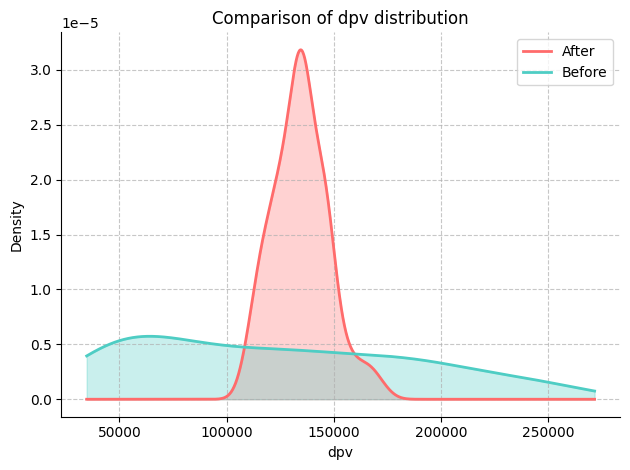

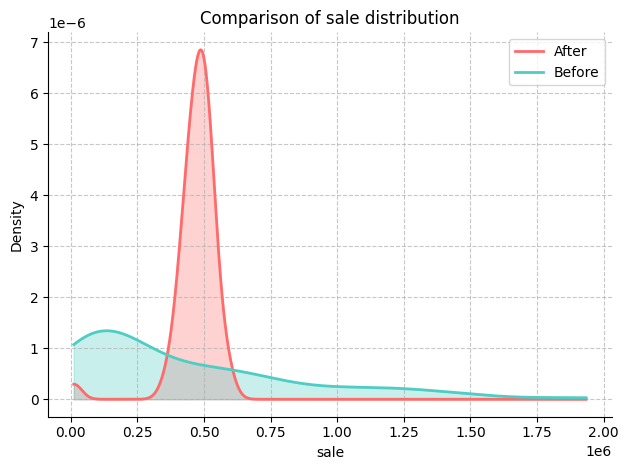

在这里,我们对 'dpv' 和 'sale' 变量感兴趣。

[5]:

# Define KPI

metric_columns = ['dpv', 'sale']

plot_metric_distributions(df_new, df_old, metric_columns)

我们可以通过比较 KPI 和潜在驱动因素的均值、中位数和方差来进一步量化变化的幅度。

[6]:

def compare_metrics(df_new, df_old, metrics):

comparison_data = []

for metric in metrics:

try:

mean_old = df_old[metric].mean()

median_old = df_old[metric].median()

variance_old = df_old[metric].var()

mean_new = df_new[metric].mean()

median_new = df_new[metric].median()

variance_new = df_new[metric].var()

if mean_old == 0:

print(f"Mean for {metric} in the old data is zero. Skipping mean change calculation.")

mean_change = None

else:

mean_change = ((mean_new - mean_old) / mean_old) * 100

if median_old == 0:

print(f"Median for {metric} in the old data is zero. Skipping median change calculation.")

median_change = None

else:

median_change = ((median_new - median_old) / median_old) * 100

if variance_old == 0:

print(f"Variance for {metric} in the old data is zero. Skipping variance change calculation.")

variance_change = None

else:

variance_change = ((variance_new - variance_old) / variance_old) * 100

comparison_data.append({

'Metric': metric,

'Δ mean': mean_change,

'Δ median': median_change,

'Δ variance': variance_change

})

except KeyError as e:

print(f"Metric {metric} not found in one of the DataFrames: {e}")

pass

comparison_df = pd.DataFrame(comparison_data)

return comparison_df

为简单起见,下文我们假设 KPI 是收入 (sale) 和产品浏览量 (DPV),潜在驱动因素包括需求方平台 (dsp_spend) 和搜索结果 (sp_spend) 上的广告支出,以及价格促销 (discount)。

[7]:

comparison_df = compare_metrics(df_new, df_old, ['sale', 'dpv', 'dsp_spend', 'sp_spend', 'discount'])

print(comparison_df)

Metric Δ mean Δ median Δ variance

0 sale 11.274001 84.089817 -95.972002

1 dpv 8.843596 12.453083 -95.913214

2 dsp_spend 6.387894 3.718354 -66.203836

3 sp_spend 10.335289 10.013358 312.605493

4 discount -1.837933 32.438169 -99.570962

2. 绘制因果图#

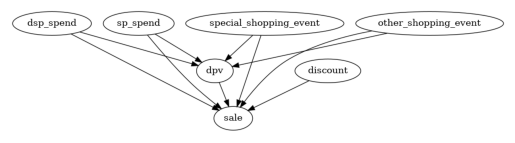

2.1. 设置基本因果图#

第一步,我们利用领域知识,认为所有广告投入和购物活动都可能是产品页面浏览量和销售额的潜在原因,反之则不然。此外,详情页浏览量也可以导致销售额,无论广告投入如何。

[8]:

edges = []

for col in df.columns:

if 'spend' in col:

edges.append((col, 'dpv'))

edges.append((col, 'sale'))

edges.append(('special_shopping_event', 'dpv'))

edges.append(('other_shopping_event', 'dpv'))

edges.append(('special_shopping_event', 'sale'))

edges.append(('other_shopping_event', 'sale'))

edges.append(('discount', 'sale'))

edges.append(('dpv', 'sale'))

causal_graph = nx.DiGraph(edges)

[9]:

plot(causal_graph)

不太可能所有这些边都显著。下一步我们将修剪一些潜在原因。这是为了得到一个更精细的因果图,即更接近真实情况的图。

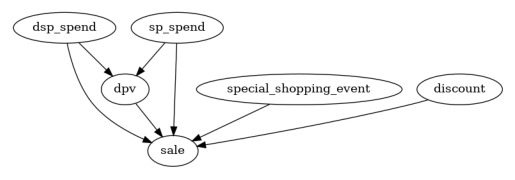

2.2. 修剪节点和边#

修剪不显著因果关系的一种方法是通过统计依赖性测试进行因果最小性检验。因果最小性检验会排除节点 \(Y\) 的任何父子边 (\(X\to Y\)),如果给定 \(Y\) 的其他父节点时,\(Y\) 条件独立于 \(X\)。如果是这种情况,节点 \(X\) 在 \(Y\) 的其他父节点之外没有提供额外信息。用通俗的话说,某些广告在其他广告存在的情况下可能不会提供增量信息。因此,我们可以移除那些 \(X \to Y\) 的边。注意,该检验已针对多重假设检验进行调整,以确保一致的错误发现率。

[10]:

def test_causal_minimality(graph, target, data, method='kernel', significance_level=0.10, fdr_control_method='fdr_bh'):

p_vals = []

all_parents = list(graph.predecessors(target))

for node in all_parents:

tmp_conditioning_set = list(all_parents)

tmp_conditioning_set.remove(node)

p_vals.append(gcm.independence_test(data[target].to_numpy(), data[node].to_numpy(), data[tmp_conditioning_set].to_numpy(), method=method))

if fdr_control_method is not None:

p_vals = multipletests(p_vals, significance_level, method=fdr_control_method)[1]

nodes_above_threshold = []

nodes_below_threshold = []

for i, node in enumerate(all_parents):

if p_vals[i] < significance_level:

nodes_above_threshold.append(node)

else:

nodes_below_threshold.append(node)

print("Significant connection:", [(n, target) for n in sorted(nodes_above_threshold)])

print("Insignificant connection:", [(n, target) for n in sorted(nodes_below_threshold)])

return sorted(nodes_below_threshold)

然后我们移除不显著的边及其相关节点,从而得到一个更精细的因果图。

[11]:

for insignificant_parent in test_causal_minimality(causal_graph, 'sale', df):

causal_graph.remove_edge(insignificant_parent, 'sale')

for insignificant_parent in test_causal_minimality(causal_graph, 'dpv', df):

causal_graph.remove_edge(insignificant_parent, 'dpv')

cols_to_remove=[]

cols_to_remove.extend([node for node in causal_graph.nodes if causal_graph.in_degree(node) + causal_graph.out_degree(node) == 0])

Significant connection: [('discount', 'sale'), ('dpv', 'sale'), ('dsp_spend', 'sale'), ('sp_spend', 'sale'), ('special_shopping_event', 'sale')]

Insignificant connection: [('other_shopping_event', 'sale')]

Significant connection: [('dsp_spend', 'dpv'), ('sp_spend', 'dpv')]

Insignificant connection: [('other_shopping_event', 'dpv'), ('special_shopping_event', 'dpv')]

[12]:

causal_graph.remove_nodes_from(set(cols_to_remove))

plot(causal_graph)

有趣的是,'other_shopping_event' 变量对 'dpv' 或 'sale' 都没有显著影响。

3. 拟合因果图#

接下来,我们需要为每个节点分配函数因果模型 (FCMs),这些模型描述了从 x 到 y 并带有误差项的数据生成过程。自动分配方法会比较每个节点的不同预测模型,并选择误差最小的模型。quality 参数控制测试的模型类型集合,其中 BETTER 表示一些最常见的回归和分类模型,例如树模型、支持向量回归等。您也可以使用 GOOD 来拟合更少的模型以加速,或者使用 BEST,这计算量很大(并且需要安装 AutoGluon)。分配模型后,我们可以将它们拟合到数据上

[13]:

causal_model = gcm.StructuralCausalModel(causal_graph)

[14]:

print(gcm.auto.assign_causal_mechanisms(causal_model, df, quality=gcm.auto.AssignmentQuality.BETTER))

When using this auto assignment function, the given data is used to automatically assign a causal mechanism to each node. Note that causal mechanisms can also be customized and assigned manually.

The following types of causal mechanisms are considered for the automatic selection:

If root node:

An empirical distribution, i.e., the distribution is represented by randomly sampling from the provided data. This provides a flexible and non-parametric way to model the marginal distribution and is valid for all types of data modalities.

If non-root node and the data is continuous:

Additive Noise Models (ANM) of the form X_i = f(PA_i) + N_i, where PA_i are the parents of X_i and the unobserved noise N_i is assumed to be independent of PA_i.To select the best model for f, different regression models are evaluated and the model with the smallest mean squared error is selected.Note that minimizing the mean squared error here is equivalent to selecting the best choice of an ANM.

If non-root node and the data is discrete:

Discrete Additive Noise Models have almost the same definition as non-discrete ANMs, but come with an additional constraint for f to only return discrete values.

Note that 'discrete' here refers to numerical values with an order. If the data is categorical, consider representing them as strings to ensure proper model selection.

If non-root node and the data is categorical:

A functional causal model based on a classifier, i.e., X_i = f(PA_i, N_i).

Here, N_i follows a uniform distribution on [0, 1] and is used to randomly sample a class (category) using the conditional probability distribution produced by a classification model.Here, different model classes are evaluated using the (negative) F1 score and the best performing model class is selected.

In total, 6 nodes were analyzed:

--- Node: dsp_spend

Node dsp_spend is a root node. Therefore, assigning 'Empirical Distribution' to the node representing the marginal distribution.

--- Node: sp_spend

Node sp_spend is a root node. Therefore, assigning 'Empirical Distribution' to the node representing the marginal distribution.

--- Node: special_shopping_event

Node special_shopping_event is a root node. Therefore, assigning 'Empirical Distribution' to the node representing the marginal distribution.

--- Node: discount

Node discount is a root node. Therefore, assigning 'Empirical Distribution' to the node representing the marginal distribution.

--- Node: dpv

Node dpv is a non-root node with continuous data. Assigning 'AdditiveNoiseModel using ExtraTreesRegressor' to the node.

This represents the causal relationship as dpv := f(dsp_spend,sp_spend) + N.

For the model selection, the following models were evaluated on the mean squared error (MSE) metric:

ExtraTreesRegressor: 166470642.14064425

RandomForestRegressor: 202413093.75654438

HistGradientBoostingRegressor: 210199781.95027882

AdaBoostRegressor: 277405500.13712883

KNeighborsRegressor: 367859348.3758382

Pipeline(steps=[('polynomialfeatures', PolynomialFeatures(include_bias=False)),

('linearregression', LinearRegression)]): 428084148.87153566

LinearRegression: 548678262.1828389

RidgeCV: 548678284.3329667

LassoCV(max_iter=10000): 557118490.7847294

SVR: 2900199761.6189833

--- Node: sale

Node sale is a non-root node with continuous data. Assigning 'AdditiveNoiseModel using ExtraTreesRegressor' to the node.

This represents the causal relationship as sale := f(discount,dpv,dsp_spend,sp_spend,special_shopping_event) + N.

For the model selection, the following models were evaluated on the mean squared error (MSE) metric:

ExtraTreesRegressor: 2332009300.2678514

RandomForestRegressor: 5154831913.930094

AdaBoostRegressor: 7802031657.73537

LinearRegression: 20252807738.720932

RidgeCV: 20398999697.143623

KNeighborsRegressor: 25224016431.708626

HistGradientBoostingRegressor: 29079555677.630787

LassoCV(max_iter=10000): 32196615412.165276

SVR: 134229564521.51865

===Note===

Note, based on the selected auto assignment quality, the set of evaluated models changes.

For more insights toward the quality of the fitted graphical causal model, consider using the evaluate_causal_model function after fitting the causal mechanisms.

[15]:

gcm.fit(causal_model, df)

Fitting causal mechanism of node discount: 100%|██████████| 6/6 [00:00<00:00, 28.75it/s]

4. 识别 KPI 变化的因果驱动因素#

为了回答过去增长驱动因素的问题,我们通过比较 2023 年和 2024 年的数据来检验任何潜在驱动因素是否导致了 KPI 变化。下文我们量化了驱动因素对 KPI 均值变化的贡献,但同样可以估计其对中位数或方差等的贡献。

[16]:

def calculate_difference_estimation(causal_model, df_old, df_new, target_column, difference_estimation_func, num_samples=2000, confidence_level=0.90, num_bootstrap_resamples=4):

difference_contribs, uncertainty_contribs = gcm.confidence_intervals(

lambda : gcm.distribution_change(causal_model,

df_old,

df_new,

target_column,

num_samples=num_samples,

difference_estimation_func=difference_estimation_func,

shapley_config=gcm.shapley.ShapleyConfig(approximation_method=gcm.shapley.ShapleyApproximationMethods.PERMUTATION, num_permutations=50)),

confidence_level=confidence_level,

num_bootstrap_resamples=num_bootstrap_resamples

)

return difference_contribs, uncertainty_contribs

median_diff_contribs, median_diff_uncertainty = calculate_difference_estimation(causal_model, df_old, df_new, 'sale', lambda x1, x2: np.mean(x2) - np.mean(x1))

Evaluating set functions...: 100%|██████████| 61/61 [00:01<00:00, 32.41it/s]

Evaluating set functions...: 100%|██████████| 61/61 [00:03<00:00, 17.95it/s]

Evaluating set functions...: 100%|██████████| 62/62 [00:01<00:00, 34.44it/s]

Evaluating set functions...: 100%|██████████| 62/62 [00:01<00:00, 34.86it/s]

Estimating bootstrap interval...: 100%|██████████| 4/4 [00:13<00:00, 3.46s/it]

然后我们可视化地绘制驱动因素对 KPI 变化的贡献,并以表格形式呈现。

[17]:

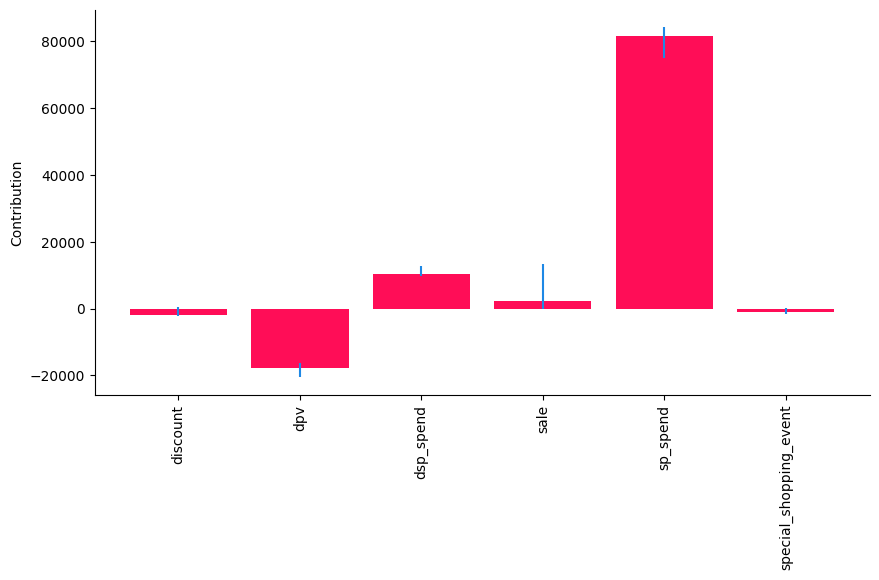

gcm.util.bar_plot(median_diff_contribs, median_diff_uncertainty, 'Contribution', figure_size=(10,5))

在这里,我们看到 'sp_spend' 对 'sale' 均值的变化贡献最大,而 'discount' 和 'special_shopping_event' 的贡献微乎其微或没有贡献。这与数据生成方式一致。

查看表格概览,根据置信区间查找显著性

[18]:

def show_tabular(median_contribs, uncertainty_contribs):

rows = []

for node, median_contrib in median_contribs.items():

rows.append(dict(node=node, median=median_contrib, lb=uncertainty_contribs[node][0], ub=uncertainty_contribs[node][1]))

df = pd.DataFrame(rows).set_index('node')

df.rename(columns=dict(median='median', lb='lb', ub='ub'), inplace=True)

return df

# show_tabular(median_contribs, uncertainty_contribs)

result_df = pd.DataFrame(show_tabular(median_diff_contribs, median_diff_uncertainty))

result_df

[18]:

| 中位数 | 下界 | 上界 | |

|---|---|---|---|

| 节点 | |||

| discount | -1810.011296 | -2351.954517 | 424.608728 |

| dpv | -17865.805004 | -20495.635150 | -16255.578160 |

| dsp_spend | 10219.005392 | 9890.028357 | 12702.789510 |

| sale | 2230.337416 | 14.939261 | 13218.827985 |

| sp_spend | 81392.392557 | 75001.284410 | 84178.124307 |

| special_shopping_event | -1019.724448 | -1713.046781 | 70.768253 |

接下来,我们移除所有置信区间包含 0 或为负数的变量,即没有清晰显著正向贡献的变量

[19]:

def filter_significant_rows(result_df, direction, ub_col, lb_col):

if direction == 'positive':

significant_rows = result_df[(result_df[ub_col] > 0) & (result_df[lb_col] > 0)]

elif direction == 'negative':

significant_rows = result_df[(result_df[ub_col] < 0) & (result_df[lb_col] < 0)]

else:

raise ValueError("Invalid direction. Choose 'positive' or 'negative'.")

return significant_rows

[20]:

positive_significant_rows = filter_significant_rows(result_df, 'positive', 'ub', 'lb')

positive_significant_rows

[20]:

| 中位数 | 下界 | 上界 | |

|---|---|---|---|

| 节点 | |||

| dsp_spend | 10219.005392 | 9890.028357 | 12702.789510 |

| sale | 2230.337416 | 14.939261 | 13218.827985 |

| sp_spend | 81392.392557 | 75001.284410 | 84178.124307 |

这告诉我们,'dsp_spend' 和 'sp_spend' 对 'sale' 的变化有显著的正向贡献。

5. 最优干预#

上面的第 4 节帮助我们理解过去增长的驱动因素。现在,展望业务规划,我们进行干预以理解对 KPI 的增量贡献。直观上,应加大投入到回报率更高的支出类型上。在此,我们明确排除了 'sale'、'dpv' 和 'special_shopping_event' 作为可能的干预目标。

[21]:

def intervention_influence(causal_model, target, step_size=1, non_interveneable_nodes=None, confidence_level=0.95, prints=False, threshold_insignificant=0.0001):

progress_bar_was_on = gcm.config.show_progress_bars

if progress_bar_was_on:

gcm.config.disable_progress_bars()

causal_effects = {}

causal_effects_confidence_interval = {}

capped_effects = []

if non_interveneable_nodes is None:

non_interveneable_nodes = []

for node in causal_model.graph.nodes:

if node in non_interveneable_nodes:

continue

# Define interventions

def intervention(x):

return x + step_size

def non_intervention(x):

return x

interventions_alternative = {node: intervention}

interventions_reference = {node: non_intervention}

effect = gcm.confidence_intervals(

partial(gcm.average_causal_effect,

causal_model=causal_model,

target_node=target,

interventions_alternative=interventions_alternative,

interventions_reference=interventions_reference,

num_samples_to_draw=10000),

n_jobs=-1,

num_bootstrap_resamples=40,

confidence_level=confidence_level)

causal_effects[node] = effect[0][0]

causal_effects_confidence_interval[node] = effect[1].squeeze()

# Apply non-negativity constraint - Here, spend cannot be negative. However, small negative values can happen in the analysis due to misspecifications.

if node.endswith('_spend') and causal_effects[node] < 0:

causal_effects[node] = 0

causal_effects_confidence_interval[node] = [np.nan, np.nan]

if progress_bar_was_on:

gcm.config.enable_progress_bars()

print(causal_effects)

if prints:

for node in sorted(causal_effects, key=causal_effects.get, reverse=True):

if abs(causal_effects[node]) < threshold_insignificant:

print(f"{'Increasing' if step_size > 0 else 'Decreasing'} {node} by {step_size} has no significant effect on {target}.")

else:

print(f"{'Increasing' if step_size > 0 else 'Decreasing'} {node} by {step_size} {'increases' if causal_effects[node] > 0 else 'decreases'} {target} "

f"by around {causal_effects[node]} with a confidence interval ({confidence_level * 100}%) of {causal_effects_confidence_interval[node]}.")

all_variables = list(causal_effects.keys())

all_causal_effects = [causal_effects[key] for key in all_variables]

all_lower_bounds = [causal_effects_confidence_interval[key][0] for key in all_variables]

all_upper_bounds = [causal_effects_confidence_interval[key][1] for key in all_variables]

result_df = pd.DataFrame({'Variable': all_variables,

'Causal Effect': all_causal_effects,

'Lower CI': all_lower_bounds,

'Upper CI': all_upper_bounds},

index = all_variables)

return result_df

[22]:

interv_result = intervention_influence(causal_model=causal_model, target='sale', non_interveneable_nodes=['dpv', 'sale', 'special_shopping_event'], prints=True)

interv_result

{'dsp_spend': 17.24967418278742, 'sp_spend': 251.46429418905464, 'discount': -0.3838008170953823}

Increasing sp_spend by 1 increases sale by around 251.46429418905464 with a confidence interval (95.0%) of [189.23222528 297.30733219].

Increasing dsp_spend by 1 increases sale by around 17.24967418278742 with a confidence interval (95.0%) of [ 2.88751799 40.04585586].

Increasing discount by 1 decreases sale by around -0.3838008170953823 with a confidence interval (95.0%) of [-1.04614227 1.0169307 ].

[22]:

| 变量 | 因果效应 | 置信区间下界 | 置信区间上界 | |

|---|---|---|---|---|

| dsp_spend | dsp_spend | 17.249674 | 2.887518 | 40.045856 |

| sp_spend | sp_spend | 251.464294 | 189.232225 | 297.307332 |

| discount | discount | -0.383801 | -1.046142 | 1.016931 |

我们类似地筛选出具有显著正向效应的干预,即具有统计显著正向回报的支出。解释是,每在一类广告上花费一美元,我们会获得 X 美元的回报,X 值显示在“因果效应”列中。

[23]:

filter_significant_rows(interv_result, 'positive', 'Upper CI', 'Lower CI')

[23]:

| 变量 | 因果效应 | 置信区间下界 | 置信区间上界 | |

|---|---|---|---|---|

| dsp_spend | dsp_spend | 17.249674 | 2.887518 | 40.045856 |

| sp_spend | sp_spend | 251.464294 | 189.232225 | 297.307332 |

这告诉我们,加大对 'sp_spend' 和 'dsp_spend' 的投入有明显的好处。请注意,这里的定量数字可能由于模型设定错误而有所偏差,但它们仍然提供了一些有益的见解。

总结#

该广告商向我们寻求帮助,以理解过去增长的驱动因素。从基于领域知识绘制的因果图开始,我们对图进行了精化,修剪了不必要的节点和边。然后我们在第 4 节拟合了一个因果归因模型,以测试哪些类型的投资变化导致了 KPI 增长。我们发现,dsp_spend 和 sp_spend 的增加都对 2024 年相对于 2023 年的 KPI 增长做出了贡献。这个结论有助于分析团队理解过去销售增长的根本原因。展望未来的预算规划,我们进行了干预,以理解增量投资回报率 (iROI),并识别出那些远高于 1 美元回报的支出类型,以便加大投入。